Forty years ago this week, reactor 4 of the Chernobyl Nuclear Power Plant exploded. The human and monetary costs were in the thousands and hundreds of billions respectively. More difficult to quantify was Chernobyl’s contribution to the collapse of the Soviet Union. However, I did re-watch the excellent HBO series Chernobyl in recent days and was struck by a non-monetary factor which might resonate for those currently enduring daily White House appeals to ignore our eyes and ears. The words of Professor Valery Legasov of Moscow State University in the opening scene of Chernobyl seem almost prescient – “What is the cost of lies? It’s not that we’ll mistake them for the truth. The real danger is that if we hear enough lies, then we no longer recognize the truth at all.” For the USSR, the truth of technological decline, an obsolete economic model, and the inability of centralised power to deal with the complexity of a more connected global economy was easy to see. But fatally, not recognized. Fast forward to today, and we could be in similar TRUTH territory….

Don’t worry, we won’t go down any conspiracy theory rabbit holes. So, no need to wonder why a would-be assassin might gain access without security challenge to the Washington Hilton and within one floor of almost the entire Trump regime senior leadership at Saturday’s annual White House Correspondents dinner. If the current head of the FBI is nicknamed “J. Edgar Boozer” then the truth is closer to incompetence than conspiracy. Similarly, but with far greater global economic impact, if Germany’s normally cautious Chancellor Merz is saying that the US has “no clear exit strategy” and is being “humiliated” by Iran, then the truth is that the US does not really “hold all the cards” or the keys to “Schrödinger’s Strait” of Hormuz. The consequences are plain to see as oil prices soar past $110 per barrel again and OPEC’s number 3 producer, UAE, just left the cartel after 59 years of membership.

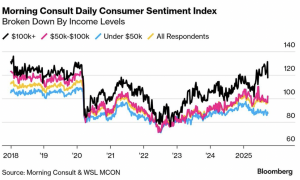

Clearly, the old world order alliances from NATO to OPEC are fragmenting. And, that’s before anyone dares to mention the eye-catching new Pew (March 2026) poll showing 60% of Americans now view Israel unfavourably — up from 42% in 2022. That’s almost as bad a swing as Trump’s voter approval on dealing with inflation shifting to a net MINUS 40, and national Consumer Sentiment surveys (Michigan/Ipsos) diving to the lowest levels seen since 1978. And yet….

There’s a danger we have been distracted and miss other truths. Watch what people do, not what they feel. For example US consumer sentiment might be plummeting but US retail sales are running ‘hot’ at 7.7% year-on-year growth, the fastest growth pace seen since 2022. Meanwhile, fossil fuels and Strait of Hormuz blockades (unless you’re a Russian oligarch’s yacht – I know…Russia, Russia, Russia) might be dominating the gloomy headlines but there’s more positive long-term developments accelerating at speed. If you have been unable to copy or track Baron Trump’s oil trading strategies or share the Fox Business congratulations of Maria Bartiromo on Eric Trump’s new $24 million contract with the Pentagon(yup), then there’s good news and bad news. The bad news is you’re not making millions on risk-free trading or commerce, but the good news is you won’t need a fitting for an orange jump suit. However, away from the fossil fuel supply crisis, check out the following quiet developments which could hurt your investment portfolio if you miss them…

- In 2025, for the first time in history, clean power met every single unit of new global electricity demand.

- Renewable energy sources (33.8%) officially crushed coal (33.0%) for the first time in 100 years.

- Electric vehicle (EV) sales in emerging markets have surged 80%.

- In Europe, EV sales soared 51% in March while EV sales smash through 25% of the total global market.

- Chinese company, CATL, just unveiled a battery with a 1,500km range that charges in 6 minutes

- China exports of batteries, EVs and solar cells were up 34%, 53%, 80% respectively last month.

A quick glance at the last two developments might suggest another uncomfortable truth; China is winning this global electrification ‘war’ and arguably is the winner of the Persian Gulf one too. However, there’s clearly only one country, USA, winning the global race for AI investment capital right now. The AI chip superstar stock, Nvidia, has just clocked up another $1.25 trillion increase in market value in less than 4 weeks. Nvidia’s current market capitalisation of $5.25 TRILLION is just shy of the entire value of Germany’s GDP and surpassed by only those of China and the USA itself. Google and Nvidia’s combined market value is now over $10 trillion.

AI is acting like a ‘death star’ for other investment sectors as it sucks up huge amounts of investment dollars. In Q1 of this year software stocks collapsed 29% from their highs while 81% of all venture capital funding ($265 billion out of $330 billion) went to AI start-ups, with 65% of that going to just 4 companies (Source: Pitchbook). You’ll keep hearing and reading that word “concentration” and how investment capital is racing into ever narrower niches within technology. However, it might be worth keeping a mix of old and new names on the investment radar. Here’s two to watch:

NEW: Anthropic, the parent of my new best work friend this week, Claude, is apparently trading in private markets right now at a $1 trillion valuation. Of course, it does help valuations if your annualised revenue jumps from $9 billion to $30 billion….in just 3 months.

OLD: Samsung, the unwieldy Korean conglomerate of TV, phone and memory chip manufacture, is going to be the most profitable company in the world by 2027. Bloomberg reckon Samsung will edge out Nvidia for top spot with a whopping operating profit of $330 billion. Yep, good old memory chips (DRAM, NAND etc) are needed by Claude, Gemini and all the other agentic chatbots to remember you (and your prompts).

So, that’s all good for now. But, let’s get back to the Truth thing. And, we’re not talking about AI chatbot hallucinations, or even Trumpolini’s Jesus delusions. It’s much more basic than that. In the middle of all this AI euphoria sits the company who kicked things off with ChatGPT, Open AI, and its CEO, Sam Altman. This week we heard OpenAI are behind on planned revenues and new subscriber growth targets. These things happen in fast growing tech stories, but OpenAI is attached to $1.2 trillion of AI infrastructure deals where OpenAI’s commitment is $600 billion despite current annual cash burn of…… $17 billion. Furthermore, OpenAI does not have a huge balance sheet like Google, Microsoft or Amazon. So, credibility and confidence matters. And, I’m concerned.

Altman’s career history per various in-depth media articles (the New Yorker one is best) is littered with massive commercial relationship breakdowns and a common theme. Loss of trust. Phrases like “profound mistrust”, “lack of candour”, “consistent pattern of lying” and “deceptive and chaotic behaviour” are used to describe the CEO of a company seeking to publicly list (IPO) in New York this year with a valuation of more than $800 billion. This week Altman faces Elon Musk in court for a $150 billion lawsuit brought by the latter regarding governance at OpenAI. Let’s just say the potential damage to Altman’s credibility could have ‘nuclear’ consequences for the AI financial ecosystem. Watch carefully and remember the fragility of the Open AI balance sheet in the context of its trillion dollar commitments. Then think of Chernobyl and Valery Legasov’s most powerful words which we have cited before on these pages…

“Every lie we tell incurs a debt to the truth. Sooner or later that debt is paid”