Dr. Tony “Holocaust” Houlihan will try and change government minds again this week on Covid-19 curtailment strategies. Change seems inevitable. Indeed, the timing of change seems to be the only area of dispute between NPHET and the politicians. In business and financial markets, change is omnipresent but again strategy shifts are often resisted. Sometimes for too long. Look at IBM which has just decided to break itself in two.

Founded 109 years ago, IBM was as recently as 1980 the most valuable company in the world. The global pandemic can’t be blamed for this remarkable strategic decision but there is no doubt Zoom was a catalyst. In recent months this video conferencing upstart has attracted a market value of over $130 billion and left IBM in the dinosaur dust at a mere $117 billion valuation. IBM spent too long defending a hardware business; the future and focus should have been cloud software. However, IBM is not alone in its strategic sclerosis.

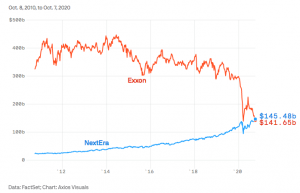

Exxon Mobile(XOM) as recently as 2013 was the most valuable company in the world. Zoom is almost as valuable as XOM but the real zinger this week was watching wind and solar power company, NextEra, surpass the market capitalization of the Rockefeller fossil fuel descendent. Quite remarkable. But, also an embarassing reminder of the costs of hubris, climate change denial and sipping the Trump kool-aid. NextEra is now the most valuable energy company in the US and the following chart painfully captures the strategic miss by XOM executives.

XOM should have gone shopping for renewable energy assets years ago. Then again shopping has changed too with Ocado just overtaking Tesco as the UK’s most valuable retailer with a £21.7 billion valuation. Tesco executives must be scratching their heads with a 27% share of the UK grocery market compared to Ocado’s hi-tech delivery share of….. 1.7%! This writer must confess to similar confusion but the chart below points to some pretty impressive confidence from financial markets:

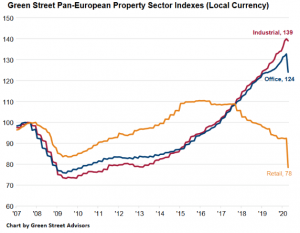

Investors have perhaps decided that retail is moving rapidly towards being a service attached to a technology platform. We shall see. However, we have more conviction, and have written so previously, in the world of banking. It is interesting to note that Europe’s relatively small technology sector has now exceeded the value of the region’s enormous banking system. See the chart below and think about that €800 billion valuation of Europe’s entire banking sector.

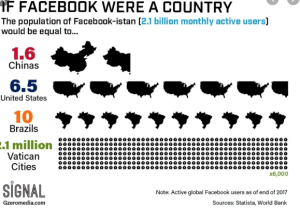

Yes, that €800 billion figure resonates with us. It happens to be only slightly more than the current market value of a single social media platform company, Facebook. How will that comparison chart loook in the years to come? We certainly won’t have to wait 109 years like IBM to see banks change dramatically. But, perhaps the more interesting question is what will Facebook look like in the next decade. Only 10 years ago we watched the Facebook start-up story, “The Social Network”. The corporate skulduggery detailed in that version was at the playschool end of the spectrum compared to what we (and most US and UK voters) know today. The ugly truth of supra-sovereign power was already apparent in this 2017 chart below:

The brutal truth is that Facebook exerts more influence than entire countries. China might be the focus of US geopolitical worries today given its huge consumer market and outsized influence on the world economy. However, one wonders will a probable Democrat President in the White House initiate a more robust discussion about breaking up Facebook. In America, the home of capitalism? Really? Never? Think again and revisit history.

In the same year that IBM was founded, another huge US monopoly was broken up. The Republican Presidency of William Howard Taft in 1911 witnessed a successful antitrust case brought by the US Justice Department against the Rockefellers and Standard Oil. What a year it was. The world’s largest company was broken up and a future global number one, IBM, began its corporate journey. However, IBM wasn’t the only global number one company to begin its corporate life that year. One of the 34 independent oil companies spun out of Standard Oil was…….. Exxon. Fuel for thought me thinks. Whither Facebook and its influencing spawn in 2021?