Here we go again; Lockdown II, and like many sequels, lacking any originality. I’ve heard some refer to this as a ‘Lazy Lockdown’, as in lazy thinking. Certainly, the one-size-fits-all travel restrictions for both urban and rural areas smacks of convenience rather than initiative. Anyway, the good news is that some business sectors have had time to prepare and hopefully battle through the latest challenges. This is a positive reminder of how commerce and capitalism finds a way forward. Not so, permanent government and the HSE who seemingly made no new plans for the seasonal return of Covid-19 and the surprisingly (not) consistent spike in non-Covid hospitalizations through the winter months…every year. Seriously, who knew? There is no sign of a fix to that perennial procrastination problem but there is better news in the business world.

We mentioned previously that commerce and capitalism finds a way. Specifically, capital has an unusually stubborn ability to flow into the economy whatever the challenge. The return of confidence and capital is critical in every downturn but what is striking about this global crisis is the huge variety of funding sources emerging; a powerful mix of the old and the very very new. Let’s start with the older funding methods first.

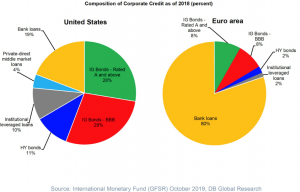

We have often stated that if one wanted to gauge levels of business confidence then watch what managements do rather than what they say. Well, companies have been writing some serious cheques as merger and acquisition activity has had its busiest summer in 30 years. Data firm, Refinitiv, has reported Q3’s combined value of transactions at more than $456 billion. The technology sector alone accounted for $226 billion of the action. Interestingly, another traditional source of deal-making capital is also making its presence felt. Year to date, private equity houses have accounted for 15% of all M&A activity per Refinitiv. We haven’t seen that level of Barbarian gate-crashing since the pre-2007 credit bonanza. It is safe to say high yield (junk) bonds still have a big fan base but it’s not just Wall Street private equity tapping that enthusiasm.

One of Ireland’s most successful (if not the most) proponent of high yield debt funding is Paul Coulson and the Ardagh Group. And, they are sounding confident. Even after two decades of deal making and a massive $5.5 billion debt load they have announced plans this week to plough another $1.8 billion into their drinks cans business. It is not just entrepreneurs with multi-decade track records receiving serious backing from the financial markets. Two young Irish companies, Wayflyer and LearnUpon, have just received almost €70 million of funding from specialist start-up financing houses in the past few weeks. One might say these are the “new” banks for smaller businesses but even the old banks are finding new missions. Check out the Big Daddy of them all, the ECB.

The EU is launching a series of 10 and 20 year bonds to fund the social needs of Member states following the pandemic and its consequences. What is extraordinary about this €100 billion programme is that the risk is SHARED across Member states and marks a departure from individual states seeking funding from financial markets. The first bond was auctioned by the ECB this week looking for €17 billion of capital. The demand was enormous with the issue more than ten times oversubscribed. Yes, almost €250 billion of demand(or a quarter of a trillion euro) wanted to fund this new experimental funding instrument. That is not the end of the new. We save the most revolutionary move until last…

We know our future is digital. But, our money? Check out the announcement from payments giant , Paypal, this week. It plans to allow users to “buy, hold and sell cryptocurrency” directly from their Paypal accounts. Yes, cryptocurrencies have been around a while but really only at the margins of everyday commercial activity. The initiative from PayPal is massive because they are massive. They have 346 million accounts globally and are annualising processed payments of close to $1 trillion. Now, one can conceivably pay for your coffee or anything else with a cryptocurrency at any of the 26 million retailers who sit on PayPal’s payment systems. Revolutionary stuff.

All of the above points to an expansion of funding channels and capitalism finding solutions to current business problems. This also signals a confidence in the scientists and an eventual vaccine for Covid-19.

Business funding is not a new thing but is always evolving, and often funding recovery. Indeed, look back to the 15th century and you will find the Medici bankers of Venice financed the Renaissance. History gives us plenty of hope. Sadly, ignorance of history (and recent winters) can do just the opposite.