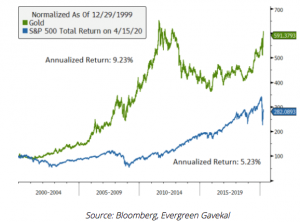

It wasn’t just the waters of East Cork glistening last week. Gold prices hit $2,000 per ounce for the first time ever too, but the barbarous relic was not the only financial asset glittering on our trading screens. The technology-rich Nasdaq index touched new record highs and Apple marched towards a staggering $2 trillion valuation. Hot stuff. And yet, the nether regions still shrank in the bracing waters of Ballycotton. Should we be mindful of Twain’s aphorism as we observe all this financial glitter? Let’s take a look at a few headlines which tweaked our curiosity.

• ‘As dollar slides, investors fret about status as world’s reserve currency’ – Reuters

• ‘Bitcoin rockets above $11,000 to year highs as dollar weakens’ – Business Insider

• ‘China’s 800 year old paper money pilot project will be ending soon’ – Forbes

• ‘Turkish lira hits record low in sharp decline’ – Financial Times

• ‘US Debt Outlook is Downgraded’ – New York Times

You will note there are no headlines in this selection above referencing stock markets but readers will already know share prices are flying from previous FAANTAM articles written here. Clearly, this is not the case with many commentators writing on record gold prices in recent days. Most have attributed gold’s recent rush to “nervous investors”. Tell that to the Robinhood investors trading an average 4.3 million times daily and chasing the combined valuation of Apple, Amazon, Google and Microsoft to over $6 trillion. For context, that number would place these four companies as the third largest GDP on the planet after China and the US. There is no fear in those expectations. Yes, there are investors investing in gold for safety but, when one views frothy corners of the stock market, perhaps there is a more nuanced interpretation of gold’s return to favour?

If we return to our selection of headlines you will note they are all very closely linked to currency markets. Currencies are the most basic store of ‘value’. Indeed, gold is often described in similar terms and historically was often used to “back” a currency. However, after the US abandoned the gold standard and the linkage to the dollar in 1971, central banks have since relied upon interest rates to manage the flow of capital in and out of a currency. Now think about those headlines capturing the emergence of digital currencies, China and soaring government debt as a challenge to the position of the US dollar. Of course, human beings are woeful at forecasting the future but this writer is inclined to wonder whether current moves into gold are driven by investors who are curious and seriously asking the following questions about the future of money…

1. Will a more insular US foreign policy ripping up international treaties on a monthly basis lead to a commensurate deterioration in the status of the US dollar as the financial system’s reserve currency?

2. Will China-US geopolitical tensions accelerate Chinese moves into digital currencies and drive capital into same from those countries wishing to trade with 20% of the planet’s population?

3. Will fiscal spending by governments to support economic recovery from the C-19 pandemic lead to debt defaults and devaluations of currencies more influential than those of Turkey, Argentina, Lebanon etc?

It is too early to answer those questions but one senses, as always, change is on its way. As the most fundamental financial asset, currency markets and their headlines are worth watching closely. Gold prices are the hint of change, not the answers. The big money must wait…..