In the investment world of benchmarks and relative performance, portfolio managers will tell you every year is a tough year. World going thrillingly gang-busters? Gotta keep pace. Risk, slowdown and volatility? Don’t blow up, survive. Arguably, for startup businesses and founders dependent on external funding support there is a similar dynamic in play.

In the giddy years, if your investment story isn’t ‘shiny’ enough you can be starved of capital which is diverted to other sectors. Then, in tougher more cautious funding environments like the last 12 months, you’re possibly juggling slower sales cycles and slower funding rounds and decisions. Worse still, no decisions. Uncertainty is a decision and business killer. And, we have no shortage of uncertainties fuelled by inflation, rocketing interest rates and geopolitical powder kegs in Ukraine and the Middle East. Now, smaller businesses and investors must deal with a fresh uncertainty coming from perhaps a surprising source, our own government.

The last US President to close out a global geopolitical proxy war was Ronald Reagan but he’s also famous for his disdain of government over-reach. In a 1986 press conference he said, “The nine most terrifying words in the English language are ‘I’m from the government and I’m here to help.’” Arguably, these words might resonate with businesses and investors currently wrangling with the latest Finance Bill and its changes to EIIS rules for equity investors and investee companies. Firstly, an easy-to-understand flat rate of 40% income tax rebates for Irish resident investors in qualifying Irish startup businesses has been chopped up into 5 different bands. The different bands, to come into effect on January 1st 2024, are as follows:

- 50% for businesses that ‘have not operated in any market’;

- 35% for a business in its first EIIS fundraise within 7 years of its first sale;

- 20% for a business in its second or subsequent EIIS fundraise;

- 20% for a business expanding into new markets or regions; and

- 30% for investments via a ‘Qualifying Investment Fund’, of which there is only one in Ireland.

Quite apart from introducing potential confusion, the ‘core’ or standard EIIS rebate of an equity investment will now be reduced from 40% to 35%. Clearly, this reduces the incentive to invest rather than increases the incentive with what could be considered particularly poor timing. We would highlight three key pre-existing factors as challenges for businesses seeking investment capital:

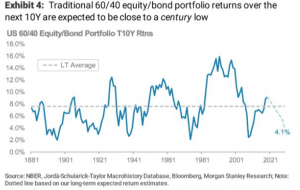

- Higher interest rates: Remember our reference to capital chasing the “shiny” things? Well, interest rates rocketing to 5% are forcing all asset classes to increase their attractiveness by offering better returns. Think deposit rates, mortgage bonds, corporate bonds and other lower risk options to earn returns. They are all upping incentives/yields while the government is seeking to make startup investment less “shiny” or easy.

- Financial Conditions: The Goldman Sachs research team tracks the broader financial climate and looks at lending patterns, terms, spreads, credit trading etc Its view on euro-area financial conditions is that they haven’t been this tight since the Great Financial Crisis (GFC) in 2008-2009. This means businesses must search harder for investment, endure tougher terms and possibly find new banking channels unless your choice is….

- Irish Banks: A senior Dublin legal eagle only recently told me that the banks are effectively ‘not open’ for any additional risk on their books before year end. True or not, the banking choices for SMEs are extremely limited as Nat West(Ulster) and KBC have pulled up sticks in Ireland and followed Rabobank and Danske Bank into retreat to their higher margin core markets.

The recent memories of Covid-19 and the pitiful take-up of the government’s Credit Guarantee Scheme (just 12% of funds used by April 2021) hint at a limited banking system which isn’t massively interested in the SME sector. As a reminder, the government was guaranteeing 80% of the €2 billion in loans under this Credit Guarantee Scheme but it seems even a 20% share of the risk was too much for the Irish banks. But, also be mindful that 99% of active enterprises in the state are SMEs and account for 70% of employment. Of course, there are other institutional sources of capital.

In the US 70% of venture capital comes from pension funds and educational endowments. In Europe, you’d be lucky if that number even reached 20%. So, despite the fabulous efforts of Ireland’s state funding agency, Enterprise Ireland, the role of private investors is critical in supporting early stage businesses. It is true that European government agencies and EU institutions(eg Horizon 2020, EIC) play a significant part and these latest EIIS changes in the Finance Bill are part of a broader harmonization of state aid. However, harmony works both ways.

Due to limited competition and regulatory constraints, smaller Irish businesses are experiencing a much more difficult banking and funding environment than their European peers. In those circumstances, one would hope that European and Irish policy makers were encouraging private capital to fill the institutional and bank funding holes. Complicating simple tax treatments is not a good start and, to add to decision paralysis, there is a critical question outstanding in the new EIIS rules.

The 50% rate applied to investments made in companies “not operating in any market” is leaving many people, both founders and investors, in the startup world scratching their heads. For us, we need to clarify the “not operating” phrase. Does this mean companies not generating revenues yet or is this demarcation geared towards companies in earlier risk stages like R&D, pre-API-type development phases? These are the questions which, left unanswered, will delay business funding and investment. Fatally, in some cases.

Now, to finish on a more upbeat note. This writer, as a long-time analyst of investments and their returns, has always been wary of treating tax rebates as a means of re-setting your starting point. In other words, if EIIS of 40% is applied, your €1,000 investment cost only €600 post your tax rebate. In my world of valuations and RETURNS the more critical point was that your investment value remained €1,000. So, in a 35% EIIS rebate world the return of your €1,000 in subsequent exit value would amount to just shy of a 54% return. If that €1,000 becomes €2,000 that’s a greater than 3x return, irrespective of whether you started with a €600 or €650 cost. That broad quantum of outcome should still keep investors very interested in startup investing. However, as we hit GFC levels of funding tightness, the government may not be able to magic up more banks but it could certainly incentivise more private investors to support the 99%. Kinda like what governments used to say they do.