The events of D-Day 80 years ago this week usually feature in the closing chapters of World War II history texts. My own current curiosity lies elsewhere, more focused on change and beginnings. Not the Reichstag fire, not Sudetenland, not Kristallnacht, not Lebensraum, not Poland. These were all events in the 1930s which historians agree shaped the outbreak of a global war. However, that decade of economic distress and social anger, whipped up by populism and propaganda, was probably inevitable. Indeed, it’s possible the seeds of war were sown much earlier. The previous decade known as the “Roaring Twenties” introduced huge economic, cultural and technology advances, but the 1929 crash and Great Depression which followed were the key catalysts for the global horror ahead. That lesson from history should not be forgotten. In fact, we should be on our guard. Welcome to the new Roaring ‘20s….

It’s not just Reddit influencer, Keith “Roaring Kitty” Gill, reportedly banking hundred million dollar profits trading ‘meme-stocks’ like GameStop in recent days. There’s more than just a sense of giddiness about. Recall the 1920’s witnessed the arrival of mass-production and mass-consumerism as automobiles, electricity, cinema, radio and aviation made technology affordable to the middle class. And, then it wasn’t. Financial collapse and the implosion of banking leverage has been a feature of global economic cycles ever since 1929. It wasn’t a once-off in 1929. The global credit crisis in 2008-2009 proved that point, and then some. The critical factors in these financial earthquakes are excessive confidence and over-estimation of demand. First let’s illustrate confidence….

- The S&P 500 benchmark index for global stock markets has not experienced a daily decline of 2% or more in 325 days (Source: Reuters).

- The market capitalisation of a media company whose key ‘product’ and biggest shareholder is a convicted felon with presidential ambitions is currently over $8 billion (Source: Truth Social – just kidding!).

- The private credit (lending) market has grown from $250 billion in 2010 to a whopping $1.7 trillion today (Source: Prequin).

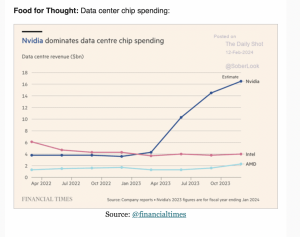

- This week AI chip maker, Nvidia, became the second most valuable private company in the world with a $3 trillion market capitalisation (Source: Bloomberg)

Regular readers will know my views fall mainly on the optimistic side of AI. However, the odd sanity-check does no harm. Nvidia is a semiconductor manufacturer. In 2023 revenues generated by the entire semiconductor manufacturing sector globally reached $526 billion. So, for context, Nvidia’s market value is now six times the entire industry’s global revenue. I know analysts will talk about future AI spend, cash rich Big Tech customers and real demand, but there’s one other aspect to this growth story which is a little bit different with historical lessons.

Legendary tech investor, Marc Andreessen, penned his “Why software is eating the world” essay in the Wall Street Journal in 2011 and there is no doubt software has embedded itself in every phone and corporation on the planet. The lovely thing about software is that it is embedded in an activity, generates recurring (frequent and relatively small) revenues and user stickiness/dependency is high. At a basic level software is code. It’s digital, not physical. Sure enough, coding platform giants Microsoft, Google, Amazon, Meta, Baidu, Alibaba etc. have dominated the league tables of most valuable companies in the world since the Andreessen prophecy. But, there has been a subtle recent shift in the value hierarchy.

Consider that two of the three largest capitalised companies in the world are now HARDWARE manufacturers (Nvidia and Apple). Hardware is physical and brings an entirely different business model and a myriad of challenges including supply chain risks, materials, energy, sustainability, customer credit, consumer fashion, inventory management and capex investment. We don’t have a crystal ball in forecasting ultimate demand for AI but the semiconductor industry used to be known for its vicious cyclicality. With my risk history hat on, I’d venture there’s every chance this manufacturing sector will experience mismatches between supply and demand. Of course, the automobiles and radios of the 1920’s might not resonate with today’s AI and technology enthusiasts. However, I’d highlight three other numbers which perhaps add to the “Roaring ‘20s” feel right now:

Sport: The breakthrough of sports like boxing and athletics on a global scale was a feature of the 1920s but fans mostly followed events by radio. Now, it’s TV (or streaming). So, when basketball’s NBA is about to treble its broadcasting deal from $25 billion to $76 billion you do wonder about excess, and the projections of Amazon, NBC and ESPN? Maybe it’s the constant circling of private equity (PE) around US sport….? Latest data from Pitchbook research shows 63 US professional sports franchises have a PE ownership connection where PE involvement is allowed (NBA, MLS, NHL and MLB). Funnily enough, basketball (NBA) leads the way with two thirds of all teams in the league connected to PE.

Securities: The 1920s saw the banks and their celebrity brokers on Wall Street begin to sell stock and bond securities to main street for the first time. Then came the ‘shoe shine’ moment in 1929. Fast forward to today’s celebrities of the private equity universe and a recent FT report on that exclusive world. The headline-grabbing data point(and possibly harsh) suggests that, in the period 2010-2023, private equity funds raised $820 billion more than they actually returned to investors (Source: Prequin).

Prohibition: Alcohol and gambling was the government target in the 1920s. So, remember when Bitcoin and its cryptocurrency ecosystem was dismissed by the ‘puritanical’ zeal of high street banks, regulators and law enforcement? Today, Bitcoin is trading above $71,000 and the total value of the crypto universe is $2.8 trillion. In fact, there are now billions of dollars invested in funds owning cryptocurrencies (ETFs) which trade daily on highly regulated public exchanges. Now, that’s a morality tale with a twist.

Of course, the reference to Prohibition conjures up images of organised crime, judicial corruption, entire city governments ‘on the take’, high profile mob trials and flagrant violations of the rule of law. Couldn’t possibly happen again, could it? Take that question with just a pinch of orange. On a more serious note, the erosion of the US rule of law is possibly a bigger threat in our immediate future than cyclical excess. Hopefully, the remembrance of D-Day sacrifice will remind those in power of their duty to call out faux (or Fox) ‘patriotism’. And, perhaps a read of the final speech in Charlie Chaplin’s The Great Dictator would help. Ironically, Chaplin’s own patriotism was questioned during a later shameful period (with my surname!) in US Congressional history. The Little Tramp’s words seem timely once again…

Let us fight to free the world – to do away with national barriers – to do away with greed, with hate and intolerance. Let us fight for a world of reason, a world where science and progress will lead to all men’s happiness. Soldiers! in the name of democracy, let us all unite! – The Great Dictator (1940)