There is one report worth a read every year. Veteran Wall Street analyst and technology investor, Mary Meeker, publishes an annual “Internet Trends” slide deck which has become a valuable source of information for business owners.

It can be downloaded at www.bondcap.com and is just the 330 pages long(!)

For those a little bit time poor we thought it might be helpful to flag a number of the key trends. Some of them might even have been covered previously in this corner.

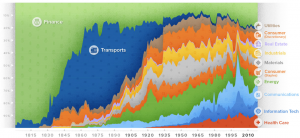

America is already great – the greatest it has ever been. Eight of the ten most valuable companies in the world are US owned and six of them are from the technology sector. As ‘Agent Orange’ in the White House threatens trade wars across the globe, readers should be mindful that only 30 years ago it was Japan who filled eight of those top 10 spots. Fingers crossed for the G20 meet this week!

Technology is the new oil. The tech sector’s phenomenal ability to scale rapidly has ensured its position as the ‘fuel” to power almost all business activities. As recently as 1980 six of the ten largest companies in the world were oil companies. More than half the human population( > 3.8 billion) is now online but user growth is slowing to a single digit growth rate of 6%.

The business future is East. The Asia Pacific region now accounts for 53% of global internet users with China and India combined making up a third of the global user base. However US technology companies are the leaders occupying 18 of the top 30 positions in the valuation tables for the global technology sector. China holds 7 of those slots but expect that to grow with its more than 800 million strong mobile user base!

Advertising spend is chasing user behaviour changes. In 2010 US consumers spent 8% of media time on mobile with mobile ad spending at barely 0.5% of total ad budgets compared to TV time and spend at 43%. Fast forward to today and mobile user time and ad spend is at 33% compared to TV at 34%. Expect 2019 to witness mobile as the top recipient of advertising spend as time spent on mobile, estimated at a daily 226 minutes, will overtake TV at 216 minutes. Also, watch out for the likes of Amazon, Twitter and Pinterest to gain additional share of those advertising revenues from Google and Facebook.

Humanity is returning to the caves. Early human communication was delivered via images/stories. Our brains are wired for images. Writing was a hack, a detour, but we are now returning to what is most natural. The principal delivery platforms of digital images, YouTube and Instagram, are gaining share of daily user time from Facebook and TV. Digital video consumption as a share of total watching time vs TV has doubled from 14% to 28% in just 5 years. Possibly more stunning is the fact that another image-based activity, interactive gaming, has become a social platform in its own right with total players now standing at 2.4 billion(!). Thank you Fortnite…..

Video didn’t kill the radio star. Arguably, voice is on the come-back trail. Podcast usage has doubled in 4 years while the Amazon Echo installed base has doubled to 47 million US users in just one year.

Banks beware. In the week that Facebook announces its own crypto-currency and Bitcoin rockets through $10,000 again the whole area of mobile payments is exploding. As European bank valuations plummet how would you value Alipay in China? This payment platform has more than 1 billion users and doesn’t just do payments; this is a full- blown financial services player providing loans, wealth management and insurance products to hundreds of millions of consumers and millions of businesses. Even closer to home, Monzo raised money this week pushing its valuation over £2 billion; and another European bank challenger, Revolut, has seen its user base double to 4 million in just 10 months.

Cloud deployment is booming. Cloud service revenues for Amazon, Microsoft and Google are growing 58% year-on-year. The cloud has also been instrumental in allowing businesses scale up using ‘freemium business models’ – Gaming, Google G Suite and Zoom are good examples where excellent free user experiences drove subscriber revenues for additional functionality. Slack in the week of its successful IPO is also worth a mention as a business service following in the footstepos of Wix, Dropbox and SurveyMonkey. According to Mary Meeker we are only just getting started with freemium business models for business and the consumer. It was gaming which proved the model – just the 2.4 billion players later and yet we are only now writing about freemium models for enterprise/businesses. Perhaps those 330 slides of Internet Trends might be worth a closer look if you want to get a better picture of the digital future of your business……

“Data is now fundamental to how people work & the most successful companies have intelligently integrated it into everyone’s daily workflow… Data is the new application.”

Frank Bien – CEO & President, Looker, 6/19