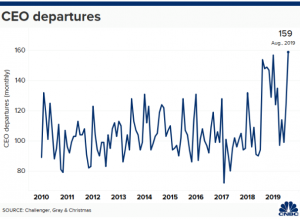

It’s not just Presidents and Prime Ministers who are looking for the exits at the moment. CEO turnover at the largest companies in the US has just hit an all-time high. While eBay and WeWork executive departures will grab the headlines it is worth noting that 159 other CEOs also left their posts in August alone.

That’s the highest ever monthly total and 28% higher than the 124 CEO exits in July. In fact, the pace of management change according to consultants, Challenger Gray & Christmas, is more than at the same point in 2008 when the global economy was about to enter a liquidity deep freeze. Clearly C-Suite anxiety is picking up when you see the following chart:

So what’s going on? Financial markets are in reasonably healthy shape, employment conditions and confidence are very robust and yes, we have a few trade war/manufacturing cycle worries. Of course, CEOs like to leave on a high(share options don’t look too shabby at the moment either) but perhaps there are a few more structural drivers involved in the mix this time.

Let’s start with the performance of financial markets and share prices. It is true that broad market indices are not far off all-time highs but a quick look under the hood would reveal a more nuanced story which we have alluded to in recent articles. To be frank, technology has been the outsized driver of positive market performance whereas the story in more structurally challenged sectors like retail, finance and energy has been far more frustrating. One senses some CEOs and Boards are becoming impatient and clutching at alternative solutions to boost share prices. So, the capital markets story has been a tale of sector haves and have-nots but there is also another inequality story.

One might wonder if CEOs are watching the rise of Trumpian populism and wondering when the income inequality backlash is coming? Note that CEO-to-Worker compensation ratio has ballooned from 30:1 in 1978 to 278:1 by 2018! That particular acceleration in uber-celebrity compensation packages stands in stark contrast to productivity gains slowing to a sub-2% annual crawl in the past decade. Perhaps the bigger problem is that worker wages have stagnated over the last 40 years but that clearly has not been a priority at board level.

The massive expansion of share buy-backs at the expense of business investment and a fixation on quarterly earnings performances has been a prevailing feature of the low interest rate monetary environment. However, that journey, as Thomas Cook employees and shareholders have discovered, can hide some pretty terminal problems for only so long. There has always been a fear that an artificially low cost of capital would lead to poor capital allocation decisions.

In this latest iteration of financial history we may look back in years to come and rue the arrival of Kardashian capitalism. Corporate failure is likely to experience the cult of CEO celebrity and short-termism starving businesses and their workers of the capital needed to transition for the digital age. Indeed, the latest data suggests CEOs are not sticking around for that final vote.

Spark Crowdfunding is Ireland’s only equity crowdfunding platform. We are based in Dublin city centre.

Our equity crowdfunding platform enables investors to invest into various stage Irish companies and it gives Irish companies the opportunity to raise new funds quickly and at low cost to accelerate their business growth.

If you are interested in learning more about Spark, then check out our website.