Freezbrury waters are imminent, but I sense things are actually hotting up. I’m also conscious it’s Friday before a bank holiday weekend so will keep it light. Let’s just highlight a few significant datapoints from the tsunami of numbers bombarding our screens this week. Then, next week we might dive deeper. Not quite as low as Cruella “Reformed” Braverman, Commandant Greg “Himmler coat” Bovino, Stephen “Peewee German” Miller, or Kristi “ICE Barbie” Noem who definitely fall into wannabe Waffen SS territory. There’s something deliciously ironic about a world which has embarked on an artificial intelligence (AI) space race while “Trump Is Making America Stupider” per The Bulwark newsletter headline. Maybe the bots won’t need to be that good? Anyway, that possibility doesn’t seem to be stalling spending by global technology giants on AI… for now.

My favourite AI datapoints this week come from Microsoft, Meta, Sandisk, OpenAI and ElevenLabs. Given these numbers are like an assault on the senses I think it’s best to present them in bullet form:

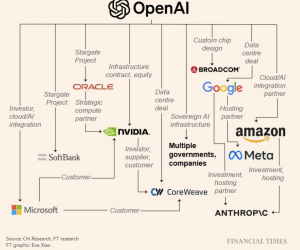

- Microsoft’s fiscal Q2 update this week showed its cloud/AI order backlog rocketing by 110% to $625 billion. But, that wasn’t the show stopper or the share price killer (down 10% overnight). A whopping 45% of that backlog ($281 billion) was linked to one private start-up company, OpenAI.

- Meta/Facebook also announced a huge number, but not a future revenue one. Its planned capital spending on AI infrastructure and development this year will be $135 billion. For context, as recently as 2023 Meta did not even generate this much money as its entire year’s REVENUES (not profits).

- Lesser-known memory chip player, Sandisk, was the S&P 500’s best performing stock last year (+577%) as a beneficiary of investors’ search for AI ‘picks and shovels’. That story continues and is a reminder not to quit on your winners. Sandisk’s quarterly update this week beat expectations with 600% earnings growth and another 25% jump in the share price in after-hours trading. So far this year, the Sandisk share price is up 127%. Yep, just January.

- In start-up land ElevenLabs is the hot AI Voice tool backed by Sequoia. It’s not just a hot investment, it’s a hot career choice. Only 0.018% of 180,000 job applicants in a 6 -month period get a job. As the brilliant VC commentator and fund manager, Harry Stebbings, pointed out, you are 200x more likely to get into Harvard.

- Back to OpenAI. Yes, people worry about that famous FT graphic and OpenAI as the potential AI investment “weakest link”. However, the capital cavalry could be on its way. Latest chat is that OpenAI plans to IPO in Q4 2026 with a raise of $100 billion on a valuation close to $1 trillion. For historical context, the previous biggest IPO raise in history was $26 billion by Saudi Aramco.

There’s now a bigger qualitative exploration of the AI theme due, given the pretty scary comments from OpenAI rival, Anthropic, CEO founder Daro Amodei. He reckons we are moving towards “AI systems that will be better than almost all humans, at almost all tasks….by 2026, 2027.” Check out the videos on social media showing how the likes of Moltbook and Clawd are blowing people’s minds with the power of their agentic capabilities. Here’s a few other mind-blowing datapoints in a variety of areas where regular readers will know I have been thematically focused.

Opportunity outside USA: We talked about real things (atoms) versus digital code (bits) previously. So, see how Brazil’s real asset-rich stock market has clocked 14% gains in January alone. However, the genuine head-rocker outside US stocks is the latest earnings growth estimates for South Korea’s stock market. Goldman’s reckon earnings growth for the entire blue chip Kospi Index will be 75% in 2026. Note most of that earnings growth will come from two companies who are critically plugged into the supply squeeze for memory chips (RAM, DRAMs, thank you Mam) – Samsung and SK Hynix. Amazingly, South Korea’s stock market is now worth more than Germany’s DAX index ($3.25 trillion).

Automation/Power Infrastructure: It’s not a huge surprise software stocks (SaaS) like SAP are being hurt by AI speculation, investment capital shifts. However, we should note the recent overtaking of SAP as the highest valued German company by Siemens. Its key three divisions? Automation processing, power/grid systems and transport infrastructure. Note none of the famous German auto stocks feature in this table-topping race.

Electric Vehicles: Europe hit an inflexion point in recent weeks. Latest data shows EVs as a percentage of new car sales overtook traditional internal combustion engine (ICE) powered vehicles. Looks like ICE on two levels this week faces an existential threat. Thinking of not nice people, it was amusing to see Tesla post a 61% decline in profits in its results this week. Who knew, apart from Ryanair’s Michael O’Leary, that idiotic interfering in other people’s business (politics and privacy too) can be brand destructive…?

Last thought, and this merits a much bigger discussion. The problems for Tesla might result in a $3 trillion mega-merger/pivot of SpaceX, Xitter, xAI and Tesla, but also subtly highlights the scale of manufacturing dominance exerted by China in the electrification race. While Trump focuses on Bruce Springsteen, White House ballrooms, Melania movies and Venezuelan oil grift, the Chinese are stealing a march on the US in so many technologies. Oh, and the Chinese consumer might be coming back. Apple just told us it had its greatest ever quarter in The Middle Kingdom. A 38% jump in China sales blew the hinges off all the ‘expert’ analyst expectations.

Lots to think about over the weekend and well done to all who invested in Social Voice before its dramatic funding close; a great illustration of investor ‘social listening’ in the venture world of little gems.