I’m nervous. This won’t win me a Nobel Peace Prize, a Pulitzer or a Green Card but it must be said. The United States is the richest, most successful and most powerful country in the world. On a global basis, we owe the United States on many levels, be it culture, sport, technology, education, medicine, defence, investment capital, tourism or friendship. Closer to home, our fortunes and miraculous recovery from a Troika bail-out are inextricably linked to US commercial supremacy. The vast majority of our pensions reflect that supremacy by holding significant amounts of US debt/bonds or stocks. EVERY pension should have exposure to US assets but risk radars are flashing red for a seismic investment shift. Behind the headlines and in the critical plumbing of the global financial system, there is increasing evidence of a global ‘exit’ from the US. That might sound odd and inevitably the counter view will cite current data which paints a record-rosy picture.

US and global stock markets are regularly hitting record highs in recent weeks. However, the US stock markets have been clocking up vastly superior returns compared to other major bourses in the 16 years since the GFC. This outperformance of US assets has resulted in extreme levels of US weightings in global indices/benchmarks which your pensions are attempting to either track or beat. A recent Deutsche Bank research note flagged IMF data showing US equities now accounting for 67% of Bloomberg’s World Index. That’s quite the weighting for a country which represents 15% of global GDP. Go back 20 years, and the US actually accounted for a higher 19% of global GDP. In 2005 US equities made up 51% of the same Bloomberg World Index. For context, Europe(EU) accounts for 12% of global GDP and 14% of the Bloomberg index. Of course, the big driver is technology stocks where the 6 top US tech companies are currently valued at $20 trillion, or more than the GDP of China. The AI/cloud (AI) revolution might be the more specific driver but is this hiding a bigger picture?

According JP Morgan’s always interesting Michael Cembalest, “AI related stocks have accounted for 75% of S&P 500 returns, 80% of earnings growth and 90% of capital spending growth since ChatGPT launched in November 2022.” AI is indeed the gift that keeps on giving for US markets. But there’s giving and then there’s giddy. I’m not sure if anyone can keep up with tech companies trying to out-do each other on the size of their investment spend announcements. It has clearly been noted by the tech C-Suite that, if you announce huge investment spend on chips, data centres or any AI related infrastructure, your share price and stock options go up. Microsoft says $100 billion, Google says $85 billion, Alibaba says $53 billion and Nvidia thinks they’ve a better twist. This week Nvidia promised to invest $100 billion in ChatGPT parent, Open AI. Excellent news but where’s the $100 billion going? Ah, that would be mostly going back to Nvidia whose AI chips will be used in Open AI’s data centres. Yep, readers might see the Baldrick-esque possibilities around circularity and vendors(Nvidia) financing customers like Open AI. Anyway, investors seem optimistic, for now. Moving away from AI, and the risk of over-investment, there’s a bigger worry for US corporates and their share prices.

The S&P 500 broke another record in recent weeks. Valuations observed by investors these days seem to ignore earnings multiples (Tesla P/E of 200x anybody?) and focus on revenues. However, there’s a traditional metric, the price-to-book ratio, which compares the market value(price) of a company to net assets (total assets minus liabilities aka book value). Where the ratio exceeds 1x, the valuation of the company is capturing ‘intangibles’ like goodwill, brand and future investment/revenue acceleration. Currently, the S&P 500 is trading at a price/book of 5.3x. That’s higher than the peak of the TMT ‘bubble’ in 2000. For context, that metric dropped to 1.6x in 2009. Of course, many companies are more ‘asset-lite’ these days and enjoy higher price/book and revenue multiples. But… there is an intangible element in many US companies’ valuation which is critically important to their premium rating over competitor companies in other countries; goodwill and/or brand power. You can see the potential goodwill problem.

I’m no Jimmy Kimmel so it’s best be straight rather than funny. Corporate America from Disney to Tesla to law firms is haemorrhaging “goodwill” and brand value. Two thirds of the global middle-class will come from India and China by 2030. Yet, right now the US assets of Chinese video platform, TikTok, are being seized/transferred to White House friendly oligarchs while India is dealing with punitive Ukraine-related tariffs (not Russia?) and a shake-down on vitally important H-1B visas for overseas technology professionals (70% of recipients are Indian). Friendly countries like South Korea are in shock after ICE raids on Hyundai’s plant in Georgia and the detainment of more than 300 Korean workers. Trump’s speech this week to the UN with “your countries are going to hell” could have been shortened to a simple message of “Go to Hell” to the rest of the world. Anecdotally, the news from Canada is a window into future “ally” consumer behaviour. Supermarket shelves are seeing a buyers boycott of many US products as car traffic across the US-Canada border craters by 34% according to latest August data. Meanwhile, corporate America and its leaders cower in silence while the Trump White House vandalises US institutions, global trade and sovereign alliances. The assault on US rule of law is captured in almost every headline emerging from Washington:

Trump’s new ABC threat proves Jimmy Kimmel right – CNN

Former FBI Director James Comey expected to be indicted on criminal charges – The Guardian

Trump pressure on Bondi to charge political foes could backfire – NBC News

US Supreme Court ruling lets Trump fire top official – BBC News

The final headline featuring the Supreme Court is critical to the risk profile of the US. Investors are worried that the Supreme Court will let the Trump regime interfere with the Federal Reserve Board, the most important financial institution in the world. The Fed underpins the status of the US dollar as the world’s reserve currency. That credibility is under threat as the dollar’s value against a basket of major currencies has fallen by 10% this year. That ‘fallen’ bit is people selling the US dollar and buying other stuff. Like Gold. Lots of investors are liking bullion’s 40% increase in value year-to-date. I’m not so sure it’s a positive signal. I’m also watching deposits sitting in US money market accounts hit a record $7.7 trillion, treble the number just 8 years ago.

These depositors are not the only ones not fully convinced about the US being the “hottest” country on the planet. Investors SOLD $3.8 billion of US stocks last week (Source: BofA Securities) with institutions and hedge funds the biggest sellers by far in one of the highest exit numbers seen this year. Oh, and if record US stock markets sound positive, context is everything. The whole world is up this year and OUTPERFORMING the US. The S&P World ex-US Index is up over 20% year to date compared to US equity markets up only 10%. But…it’s worse than that if you factor in US dollar weakness. Returns for overseas investors in US equities are closer to ZERO this year. To be clear, this re-rating of US assets will happen over years not weeks but commercial contracts, the law and international treaties require a high degree of confidence. Imagine how Canada and Mexico feel right now re-negotiating a deal which Trump himself shook hands on as recently as July 2020. His own deal. Investors will deal too, and consider a sea change in how the US attracts talent (H-1B, visas), investment capital (Fed, US dollar) and goodwill (premium equity ratings). Sadly, US-based investors might struggle for similar analysis in their media.

Despite Trump railing against windmills (literally) and media bias, the awkward truth is that the wealthiest person in the world, Elon Musk, owns Twitter/X. The second wealthiest person in the world, Larry Ellison, owns Paramount(including CBS) and will now be taking over TikTok and CNN. Jeff Bezos owns The Washington Post and Twitch. Mark Zuckerberg owns Facebook and Instagram. Throw in Larry Page as Google’s controlling shareholder and that looks like the top 5 richest men in the world are ALL media owners. It also looks like oligarchy. US corporate leaders should also consider another consumer shift within the borders of the US.

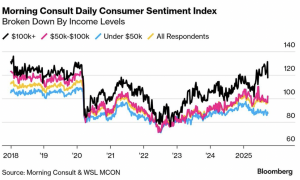

Research from Moodys using Federal Reserve data shows the top 10% of earners in the US now account for 50% of all consumer spending. In the early 1990s (before Fox News) that number was closer to a third of all spend. Disney just discovered (as corporate America said zippo) that the average person felt that taking a comedian off air after government threats was plain un-American, and proceeded to cancel in massive numbers their Disney+ and Hulu subscriptions. Maybe, the 90% will push back on other White House over-reach? I’m not so sure, and that’s not good for US assets or pensions in the long run. Investment securities, after all, are contracts and the undermining of the rule of law will end in tears. Or, something less oligarchic. As my favourite bear strategist, Albert Edwards, said this week when posting the Bloomberg chart below, “When I look at this chart, I look at my calendar and just wonder when I should pencil in the next revolution..” The chart dramatically shows consumer sentiment splitting sharply between the ‘have yachts’ and ‘have nots’…..