I know, I know we’re not supposed to throw the “F” word about lightly. But things are getting serious, and expletives aren’t even close to what I’m thinking. I’ll save those for counting freezing Freezbrury water minutes. No…my reluctant F word is FASCISM. Possibly over-used in recent times….until now. Check out the enormous banner poster of Donald Trump which has just been hung on the outside of the headquarters of the US Justice Department (DOJ). Gobsmacking. The capture of the rule of law in the US is now almost complete. While business leaders are removed, senior foreign government officials resign in disgrace and the 8th in line to the throne of the UK is taken into police custody, Trump’s private legal firm (the DOJ) is desperately trying to deflect and pretend there are no US-based Epstein predators. Deflection tactics from the White House have now moved on to releasing files on Aliens (the non-ICE versions) and UFOs. However, the biggest ‘bread and circus’ deflection show is the 15- day countdown to conflict with Iran.

I am struck by how complacent current geopolitical risk thinking is right now, and what desperate measures Tehran’s murderous regime might take to strike a blow against the US and its allies in the region including Israel. Any regime which murders 20,000 of its protesting citizens in a matter of days is capable of awful stuff. So, it concerns me that the emotionally stunted “Admiral Bonespurs” in the Orange House and his War Secretary, “Whiskey Pete”, in the Pentagon will be the key decision makers if US forces take larger casualties than expected. We are into very unpredictable territory now. However, Iran is not the only risk reality creeping up on us.

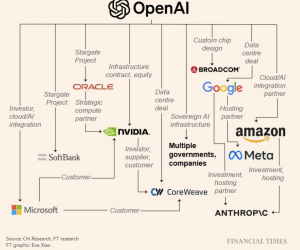

The financial markets have been focused on the carnage wrought on software company share prices year-to-date. Valuation destruction has been close to $2 trillion as the latest Wall Street thinking is that AI will blow up software business models. It even has its own event taxonomy – “SaaSpocalypse”. The basic premise is that companies will build their own workflow, HR, process applications etc. in-house with increasingly powerful AI coding tools. Thus, software companies could face growth and competition challenges which in turn impacts valuation/sales multiples framing that growth. In fact, this invasion of artificial digital expertise is in danger of commoditizing software. Ironically, there has been a complete reversal of the valuation hierarchy between hardware and software. In tech terms, things are getting very real. Real stuff like memory chips(DRAM) and logic chips (GPUs) are perceived as supply constrained and ditching their historic ‘commodity-type’ characteristics. The best illustration of this shift in investor perceptions is the stunning statistic that 89% of semiconductor companies’ (real stuff) share prices are flying (trading above 200 day moving average) while precisely ZERO software company (digital bits) share prices are exhibiting any technical strength(evidence of buying). However, we are in danger of focusing on the trading trends of financial markets while missing the bigger AI picture. Technology insiders are becoming more nervous about the power of AI without adequate guardrails…

It’s difficult to get away from Anthropic’s founder, Dario Amodei, confidently predicting a world where AI systems would be “better than almost all humans at almost everything” within 2 years. Implicit in this forecast is the rapid realisation by the rest of us that AI systems are soon going to be coding their own optimised functions. If you’re thinking Terminator and Skynet you wouldn’t be far wrong and we’ll definitely need more than Arnold this time. As the global geopolitical balance shifts towards lawless autocracy and fascist ‘might over right’, we seem as a species particularly ill-equipped for what’s to come. Amodei himself describes the challenge:

“Humanity is about to be handed almost unimaginable power, and it is deeply unclear whether our social, political, and technological systems possess the maturity to wield it.”

It feels like a moment of AI truth is approaching. If I were to strike an optimistic note, I’d be encouraged reality is beginning to break through to the public consciousness on a number of fronts. This could bring a very welcome return to valuing credibility, data and honesty. Populists beware and feast your eyes on these beauties:

Brexit: The UK’s Office of Budget Responsibility (OBR) has estimated the various costs of Brexit at 6-8% of GDP, £100 billion per year of structural economic losses, 4% productivity loss and 15% lower trade volumes.

US Manufacturing: All the trade shakedowns, foreign investment ‘promises’ and noise about making America manufacture again (Oh Mama!) resulted in 2025 manufacturing/factory construction spend actually FALLING by 7%. Oh, and the US has lost 70,000 manufacturing jobs since tariff ‘Liberation Day’ last April.

US Trade: Just in…. the US trade deficit remained a stubborn $900 billion in 2025. That’s a microscopic 0.2% reduction in the deficit despite all the ‘winning’ and tariff chaos trumpeted by Agent Orange. And now for more breaking ‘winning’ news…. The Supreme Court of the United States has reportedly ruled, in a 6–3 decision, that tariffs imposed by Donald Trump were illegal. The ruling could leave the U.S. facing more than $150 billion in potential tariff refunds.

That final datapoint of almost zero deficit reduction is just embarrassing. But it gets better. Shockingly, to nobody outside the US, other countries trading with the US are smarter than Howard “Nutlick” and his Commerce Department lackeys. The US trade deficit with Taiwan is now bigger than that with China. The last time that happened was in 1992!! It seems like the rubber is meeting the road for quite a few of these populist distractions. Indeed the final irony, 250 years after the US gained its independence, might be that the epic downfall of a British prince reveals the true colours and deceptions of a ‘King’ in Washington…..