The weather forecast isn’t great. I’d usually suggest some couch thinking time but that phrasing has now become a politically-charged innuendo in the US which tops off possibly the most bizarre presidential campaign month ever. Don’t ask about couches or dolphins, or JD Vance. And, he thought having no children was the problem…..! Anyway, given the amount of delusion in the air, I’m going to suggest a beach plan. That might be the wrong plan, but thematically we might be on the right track in the world of finance. So, for those enjoying some time off, one can review and reflect on the following:

Old economy: Our suggestion “Investors Need The Old Economy Too” in May started subtle, then went full hammer. This move hasn’t just been a tech shift from software to more traditional hardware manufacturing. Say hello to the ‘great rotation’. The old economy stocks roared in July. The top performing sectors in the US were industrials, financials, utilities, basic materials and real estate. As an illustration of the scale of rotation, note technology stocks actually had a negative month (-2%) while US regional banks and housebuilders rocketed 19% and 17% respectively.

Smaller companies: We have written “Betting On Small Can Really Win” but boy oh boy did it rock in July. Smaller companies tracked by the Russell 2000 index whipped the performance of the large company S&P 500 by 10 percentage points. That’s the largest monthly divergence between size cohorts ever recorded in history.

Climate and cleantech: Another theme close to our hearts. VC Breakthrough Energy Ventures backed by Bill Gates has just raised the largest climate fund of the year with a funding round of $839m. In Europe, the momentum is good too. Private equity deal values in European cleantech are now on track for their best year ever(Source: Pitchbook).

Fintech: Stripe and Revolut valuations in recent private share sale activity have jumped by 40-50% and London remains a fintech investment hotbed. Latest British Business Bank data tells an interesting City story – the UK fintech sector is attracting 11% of global VC investment (and 48% of all investment in Europe), a share only exceeded by the US.

UK Comeback: In March we wrote “Time For A UK Recovery” and waited for credibility and competence to return to Westminster. The scorecard at the moment looks pretty good: UK equities are seeing the strongest inflows of foreign institutional investment for years (Source: BOA), and on the currency front, the GBP (formerly known as the “Great British Peso”) has been the strongest major currency performer in the year so far (Source: Bloomberg).

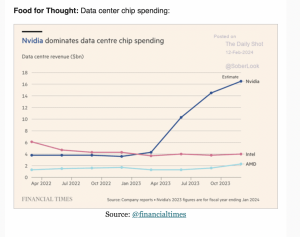

Digital infrastructure: We wrote “Get Ready For The Cloud Wars” back in November and this has morphed into a global foot race to acquire, invest, service and build the infrastructure of our digital/AI future. From data centres to state-of-the-art chip manufacturing plants the investment giants are moving fast to get involved. While Microsoft opens a data centre every three days, it feels like the likes of Blackrock, Apollo and Blackstone are competing for digital infrastructure headlines every few days too. In fact, Blackstone estimate digital infrastructure spend by top tech companies will exceed $1 trillion over the next 5 years.

Wall Street veterans would say ‘the trend is your friend’. So, we aren’t giving up on any of these themes just yet. However, we will return to two critical risk factors for many of these themes in a later article. Geopolitical risk from Taiwan to Iran to US electoral chaos looks like it is escalating rather than fading. US politics can make for electric watching (with the shock too) but the just announced prisoner swap deal between Russia and the US was significant. The allied multinational effort by the Biden White House shows the value of joined up thinking and shared values but the planet faces other bigger challenges. Arguably, our highly charged politics needs to address the fundamental challenge of climate and electricity too. For another day, but the race to decarbonise and electrify the global economy is definitely not on track…..