Sixty years ago a frail 46-year old man descended the steps of a modified Boeing 707 at Dublin airport. The American visitor was blessed with film-star good looks which disguised debilitating back pain and a potentially fatal Addison’s disease. He also hid his and a nation’s fears. The Cuban missile crisis of the previous year was a domestic reality check on the seemingly unstoppable global expansion of the USSR and totalitarianism. Elsewhere, but in the same hemisphere, the majority of South America’s sovereign states were about to embark on a dramatic shift from democracy to one-party rule. In Europe, the Berlin Wall was built overnight in 1961 and South East Asia’s dominos were already beginning to wobble with South Vietnam in the cross-hairs of Ho Chi Minh’s North Vietnam and Mao’s China. But, it wasn’t just political retreat as civil rights tensions brewed and extremist assassins plotted. Economically, the USSR was the fastest-growing economy on the planet, bar Japan, in the 1960s. Its GDP was approaching 60% of that of the US as the 2nd ranked economy in the world and on its way to beating the US in the space race with an unmanned lunar landing in 1966. And yet, John Fitzgerald Kennedy, 35th president of the United States, enjoyed approval rates at home of more than 80%. Oh how President Joe Biden could wish for similar approval rates this week. A warm Irish welcome will have to suffice, even rhyme with 1963, but do our fears rhyme too?

As always, we look to flows of investment capital as data points and clues to what real money fears. The Financial Times this week referenced EPFR data to show global investors have pulled $34 billion from US equities funds so far this year. In contrast, European($10 billion) and Chinese equities($16 billion) have experienced inflows. Of course, the commentariat has been quick to suggest the recent collapse of Silicon Valley Bank and Signature Bank could be just the beginning of credit turmoil, possibly triggered by the falling values of office real estate. Others are even suggesting the recent agreement between Brazil and China to ditch the US dollar in trade deals means the greenback is in trouble and in danger of losing its status as the world’s currency reserve. I struggle to see those fears destabilising the US banking or monetary system. However, I am conscious of another economic metric. Currently, the US stock market accounts for circa 43% of the $96 trillion invested in equities globally (Source:SIFMA). The blunt commercial reality is that the US corporate investment pool is four times bigger than its next biggest challenger, China. Stock markets do not necessarily reflect economic cycles, politics or even GDP. They represent business confidence, innovation, returns on investment and…. the rule of law. And, I have a few fears. Two big ones actually.

- The rule of law: Whether Trump or his hundreds of co-grifters end up in orange jumpsuits is almost irrelevant, and certainly backward looking for equities markets. What is far more worrying is when the judicial system, and established law, is undermined. So, imagine how every corporate leader felt this week when a Trump-appointed federal judge in Texas invalidated the FDA’s approval of an abortion pill, mifepristone. Yep, it’s been on the market for 23 years but Justice Matthew Kacsmaryk has imposed a nation-wide ban on mifepristone sales based on a random sample of blogging views and his personal ‘expertise’. The denial of science and FDA expertise was worrying enough to drive the executives of 500 pharmaceutical companies to sign a letter condemning the judicial over-reach. This ideological attack on federal authority and decades of scientific evidence has the potential to put approval of all drugs at risk, and seriously impact innovation and returns in an already risky investment space. If one thinks it’s just the healthcare industry under assault, think again.

- Investment returns: Previous articles here have referenced attempts by Republican legislators to attack “woke” fears on the global climate crisis and ESG initiatives . The Republicans’ eager embrace of fossil fuel industry donations has triggered a flurry of anti-ESG legislation forcing state government bodies to cease business with investment firms who use ESG criteria as part of their selection process in deploying capital. Texas and Florida have been in the forefront of this “woke” backlash but as Blackadder might say to Baldrick, “there’s a tiny flaw in that cunning plan”. It turns out that retirees and taxpayers would end up paying more for capital to fund their pensions, infrastructure, government services, utilities etc. if there were fewer purchasers of state securities/debt. Funny ‘ol game, this investment thing. Sure enough, Kansas, Wyoming, North Dakota and Indiana have shied away from their original legislative plans to go full MAGA on investment managers trying to save our planet. More bizarrely, for the larger states like Texas and Florida, there is this Kafka-esque intrusion on all investment activities. As the more thoughtful legislators have quite correctly pointed out, forcing companies either to ignore ESG or to invest in fossil fuel energy can both be capable of damaging investor returns. Not surprisingly, big investment firms are calling out the lunacy, but uncertainty reigns and that’s not where capital wants to be.

So, in a nation of threatened legal precedent and uncertain returns, the critical stock market component of confidence could be structurally undermined. A structural shift in confidence could have an impact felt over decades but there’s a part of me and history which provides some cyclical comfort. President Biden’s approval ratings are in the low 40 percents despite US full employment, US global technological dominance, US capital markets leadership, dramatically improved US ‘soft power’, the demise of its most significant military super-power rival and a strengthened NATO. What’s not to like or…… fear? Well, turn on Fear-Fox news and the borders are overwhelmed, apple pie and the 1950s are gone forever, inflation is never falling, family values are fading away(but not AR-15s) and business owners are drowning in regulations. However, the average age of a Fox news viewer is 68-years old and, if truth(!) really be told, they are not the future. In reality, the following developments are far more likely to impact the voters and surveys of tomorrow….

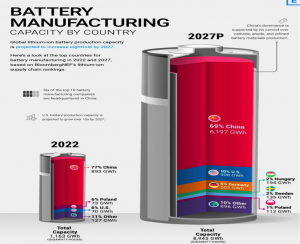

US Manufacturing: The Biden Inflation Reduction Act was passed in 2022 and is looking like the most revolutionary economic policy seen in 60 years. Incentives to bring manufacturing capacity back to the US, protect the microchip industry and turbo-charge cleantech investment has resulted in $52 billion of investment in factories alone. Cue the Wall Street Journal headline “America is Back in the Factory Business”

US Technology: Steve Jobs once said computers were “like a bicycle for our minds”. American innovation, immigration, and investment has delivered a global digital dominance which now accounts for 24% of the value of US stock market indices. But what about artificial intelligence(AI) or even generative AI? It is entirely possible we are staring at a potential Ferrari for our minds. There are plenty of fears out there about AI replacing humans but one suspects those that grasp the potential of human-prompted AI will deliver massive wins for humanity in healthcare, education, medicine, energy savings and retirement-care. With a bit of leadership the US is perfectly placed to capitalise.

And voter approval polls can be cyclical too. Kennedy didn’t live to see Apollo 11 on the moon in 1969 but he did say the US would get a human there first. The benefits of that space race in accelerating computing power, business innovation and military superiority cannot be underestimated. One wonders could a new vision or target inspire? We shall see but for any of you who watched the shameful scenes in the Tennessee Statehouse in the past week there was an uncanny 1960s feel about the footage of young idealistic “Tennessee Three” legislators standing up for school children and what is right. The words, the look, the tone and the passion of Representative Justin J. Pearson are worth a watch. Then watch hopefully, not fearfully, for a Biden presidential vision to gather momentum and rhyme again.