And I thought government advice to do pantos with no kids would be the most confusing thing this week. But no, the wider world continues to bewilder and generate even stranger headlines than my favourite tabloid one of recent days – “Sweet Jesus, Mary and Joseph… and the wee Donnelly.” Back to my line of duty in identifying change/risk… I’m thinking about Generation Z a lot these days. Every business is too. But let’s kick off with some interesting developments and probable confusion.

The Turkish lira may be collapsing but Salt Bae, the Turkish celebrity TikTok chef, has embraced the world of inflation rather enthusiastically. Wagyu beef ribeyes encrusted in 24-karat gold leaf are being gobbled up by London diners at $1,000 a pop. No seriously – they eat them, they don’t collect them. On so many levels I struggle with that but then I came across another Turkish artiste. Meet celebrity digital designer, Murat Pak, who has just finished the largest primary sale by any living artist in history.

Over the past weekend Pak sold 266,855 pieces in his “merge” collection for between $400 and $525 each to realise total auction proceeds of over $106 million. I’d use exclamation marks but having viewed some of these digital art works I’m tempted to charge for punctuation in my own online endeavours. Do take a peek. You’ll see what I mean and possibly share my confusion. These digital art works are non-fungible-tokens(NFTs) which certify digital ownership. But there’s more, lots more coming.

Total NFT annual sales in art, collectibles, luxury goods and gaming are currently hitting $20 billion. That sounds like a big number but then consider the gaming industry alone is a $180 billion annual revenue monster which is three times the size of the art world. Bluntly, NFT penetration of real life experiential activities is only just beginning. If we include the $1 trillion retail fashion market then the total addressable real life market is closer to $2 trillion. Now we’re talking trillions but that’s old news to cryptocurrency followers.

Cryptocurrencies like Bitcoin and Dogecoin might be suffering some volatility of the downside variety in recent days but it seems inevitable that the crypto universe will expand again. The most recent high water mark for the value of the total crypto complex was $3 trillion. Now if we add in the potential NFT addressable market of $2 trillion we’re already talking about a universe larger than Japan’s annual GDP. I mention a sovereign nation deliberately because it has been suggested in some commentariat circles in recent weeks that we should think of crypto/NFT total values in terms of GDP. That almost makes sense from a broad economic activity/monetary circulation perspective but I believe we are going to have to re-consider how we quantify GDP soon enough.

Forget Leprechaun economics and multi-national boosted GDP. What about Squid economics? The impact of Korea on Generation Z culture has been phenomenal. Back in 2019 Parasite became the first non-English language film to win the Academy Award for Best Picture. However, the true trail-blazer was Korean pop music or K-Pop which started out in the early ‘90s as slickly choreographed dance routines, eye-catching outfits and polished lyrics. The K-pop band, BTS, are possibly the biggest band on the planet and an entire industry has grown up around this musical genre. Spotify has reported K-pop downloads rocketing by 1800% since 2014 but it might be Netflix who are truly smashing it with its Korean cultural contribution.

Its hit survival drama, Squid Game, has been watched by a whopping 142 million people and its value to Netflix has been quantified at over $900 million. No wonder the Korean Ministry of Culture has been investing heavily in cultural exports, or as they call it “Korean Wave”. Squid economics or not, audiences are clearly enjoying different things these days. And yes, fashions and behaviours change. However, it should be noted that two thirds of the world’s middle class will be living in Asia by 2030. Many will have been born after the end of the Cold War and that feels like a significant cultural and demographic inflection point. It should also be noted that changed and unfamiliar behaviours are not just a Generation Z phenomenon. Time to look in the mirror Boomers.

Older generations might sneer at the €3 billion of venture capital coming into crypto investments in the past month alone but there are far bigger pools of more mature capital potentially venturing into euphoric territory. For every Bored Ape Yacht Club or CryptoPunk digital image selling for $200,000 there’s potentially a real world chart out there which should cause pause for thought. Here are three real life images which caught my eye in recent days:

- The publicly listed technology sector is the real life equivalent of a Salt Bae steak. More specifically, the valuation of the technology sector relative to the rest of the market is now back at the peak TMT bubble levels of March 2000. Pets.com meet Bored Ape meet Tech 2021….chart courtesy of Bloomberg:

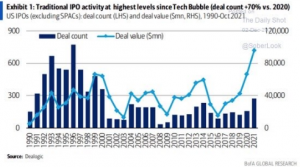

- IPO activity is also back at bubbly 2000 levels in terms of deal value. It is important to note that in a typical IPO transaction there are people actually choosing to sell at that moment in time. That happens every day but the risk dial tends to move when activity deviates from historical norms. US public listings alone have generated more than $1 trilion of IPO proceeds. See the Bank of America graphic below and note that if you included special purpose acquisition companies (SPACs) then the deal count would be considerably higher:

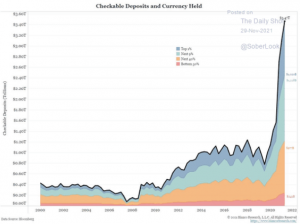

- Perhaps all this activity is part of the global search for “yield” by savers struggling with rock bottom interest rates and inflation eating into the purchasing power of their cash deposits? Clearly, central bank support of financial markets has increased investor confidence but, as previously mentioned, investor behaviours can be difficult to rationalise these days. Cash might be defined as a low risk savings option but, with possible negative interest rates and inflation, savings capital can still suffer serious damage. However, the next chart highlights a staggering behavioural split between rich(older) and not-so-rich(younger). The top 1% of US households in this Daily Shot/Bloomberg graphic have gone full “tin hats on” in their cash deposit accounts but actually could be running huge capital destruction(inflation) risks:

So, arguably there are similar pockets of unusually risky behaviour in both Gen Z and older age cohorts. Dare we say these generations are more alike than we thought? Think again. A 2020 global survey by WordPress found that Gen Z consumers want brands to be “fun”, “authentic” and “good”. We will return to “fun” but the “good” bit resonated in recent weeks as this survey highlighted that 72% of Gen Zers are more likley to buy from a company that contributes to social causes. Anyone for tennis? In China?

Not the Women’s Tennis Association(WTA) who have just pulled all tournaments from The Middle Kingdom. I use the medieval name deliberately. The WTA concern is the welfare of sexual harassment victim and top ranked professional tennis player, Peng Shuai, who has been silenced and has probably lost her right to travel freely. My concern is that no major consumer brand with Chinese commercial interests seems to give a toss. The moral gymnastics required to keep both China and $50 trillion of sustainability/ESG influenced capital on board will eventually end up with some broken brands. And…Gen Zers just won’t play ball(!).

Gen Zers won’t work like older generations either. Covid-19 let the genie out of the bottle – fun and work-life balance are possible if you work for yourself it seems. The US Census Bureau is reporting record-high figures for new business formation through the first 9 months of 2021 and this begs the question as to how could investment behaviours change to reflect life priorities(climate, brands, do good) and fun? We shall return to this question in a later article in more depth but will leave you with one inter-generational commercial clash which prompted some early thoughts.

Some readers may have read about an attempt by 17,000 people to band together to buy an auctioned copy of the US Constitution. They raised $40 million and narrowly lost out to Citadel hedge fund titan and retail trading hate-figure, Ken Griffin. Cue total consternation and confusion as to how the cryptocurrency denominated(Ethereum) money raised could be returned to individuals. But now, those same tokens ($PEOPLE) are pricing higher than prior to auction. I won’t try to rationalise that scenario but three things struck me about the potential future of investment:

- Traditionally, investment has been conducted through centralized institutions like Blackrock, Citadel, Goldman Sachs etc. The US Constitution auction at Sotheby’s was contested by a Decentralized Autonomous Organization known as a ‘DAO’ in Web3 circles. Almost like an investment “flash mob” this non-hierarchial group was formed with one mission. My sense is that there will be more of these. Why?

- Fun and community experience is a big part of Gen Z thinking. Financial return might be the wrong way to initially think about a Gen Z purchasing decision but the subsequent scarcity value of being involved in a social-values mission could be extremely high. FOMO meets values credibility.

- When I look at league tables for the performance of asset classes in 2021 I see almost everything on fire – oil, commodities, food, equities, venture capital, crypto etc. And gold, the ultimate inflation hedge? Yep, it’s actually down this year. We should consider the possibility that entire asset classes or sectors could be ignored by Gen Zers in the future. Who wants to be a billionaire? Maybe those who avoid gold, China, fossil fuels and water guzzling food.

All a bit revolutionary for you? Well. Let’s go back a bit to the ultimate anarchists. Steven Johnson , author of Where Good Ideas Come From, flagged that the pirates of the 17th and early 18th – century were pioneers of trialling new models of governance and wealth sharing. Before each voyage there were “articles of agreement” and a very egalitarian share of future profit among the crew. These mini-constitutions pre-dated both the American and French Revolutions by nearly a century but were clearly ahead of their time in terms of separation of powers, insurance and leadership change. Indeed, after the January 6th Insurrection in Washington you might argue some of these later documents of democracy need updating. However, the more important point is that we should watch the evolution of these Gen Z DAO initiatives carefully. They could be an early window into our financial future, our values and our valuations.