I love Sarah Cooper. Not long ago Sarah was writing articles for the Financial Times. Now she’s a TikTok star. Her hilarious use of the lip-sync video app to ridicule Donald Trump’s daily vomit of gibberish have been social media gold. Needless to say, the Donald has been less impressed and one can only wonder what the true motivation for his most recent executive order.

The thin skinned Toddler-in-Chief has ordered the Chinese corporate parent of TikTok to sell its US operations citing security concerns. Sarah will be fine – she has just secured a contract for a Netflix series – but there’s a potentially much bigger impact. The Trump administration is also demanding that US firms sever commercial links with another social media platform, WeChat, owned by a Chinese parent.

WeChat is the Chinese equivalent of Whatsapp, Instagram and Facebook all rolled into the one app. It is commercially critical for any company with Chinese customers. Surveys already confirm iPhone sales in China would evaporate if Apple was unable to support WeChat on its devices. Is this the next phase of the technology decoupling between the planet’s two largest economic powers? If so, what next? Financial markets might already be providing a few clues.

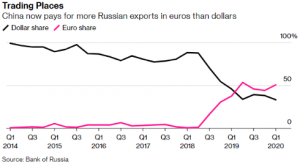

The currency markets are seeing some interesting moves. Not long ago the Trump regime was all talk about building a wall to keep immigrants out. It turns out, thanks to a spectacularly bad management of the C19 pandemic, that the rest of the world now wants its own wall to curtail the cross-border travel of American citizens. As US infection rates over the past 3 months climbed to the 5 million mark it has been noteworthy to see the euro strengthen by 10% in the same period compared to the US dollar. More striking was this chart below from Bloomberg showing the Chinese now paying for more Russian exports in euros than in dollars.

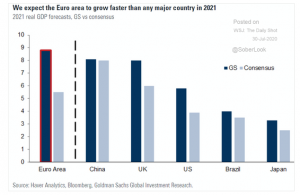

The new-found enthusiasm for the euro might be a relative vote of confidence in a post-pandemic recovery. Goldman Sachs thinks the Eurozone economy will grow faster than any other major country next year. The next chart tells that story.

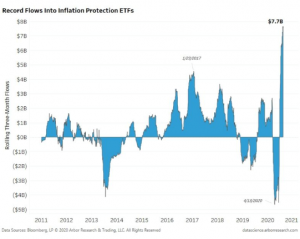

Of course, growth stocks have dominated the headlines in 2020 as technology sector valuations have rocketed and clocked our first $2 trillion company, Apple. Cheaper, more traditional old economy stocks have struggled to perform for a decade. Europe, with a relatively small technology sector, has lagged too. But whisper it softly, old economy(value) and European stocks could benefit from the “i” which hasn’t really been seen since the iPhone arrived. We are seeing signs of investors protecting themselves from….. inflation. An early vaccine(I’m hearing lots about October) and $10 trillion worth of central bank pandemic pumping is a juicy inflation combo and might explain this chart of record buying levels in inflation protection instruments(ETFs):

Time will tell on inflation but one thing is almost certain. The unwind of Chinese-US trade and internet connectivity is set to continue. TikTok might have 45 days to comply with Washington’s demands but investment capital can move even quicker. Like right now. The charts above suggest that capital is ready to sync with Europe. Cue Ms. Cooper, Netflix and the theme tune from ‘Curb Your Enthusiasm’ with footage from the White House bunker……